Quick answer: eCommerce furniture market size in 2026

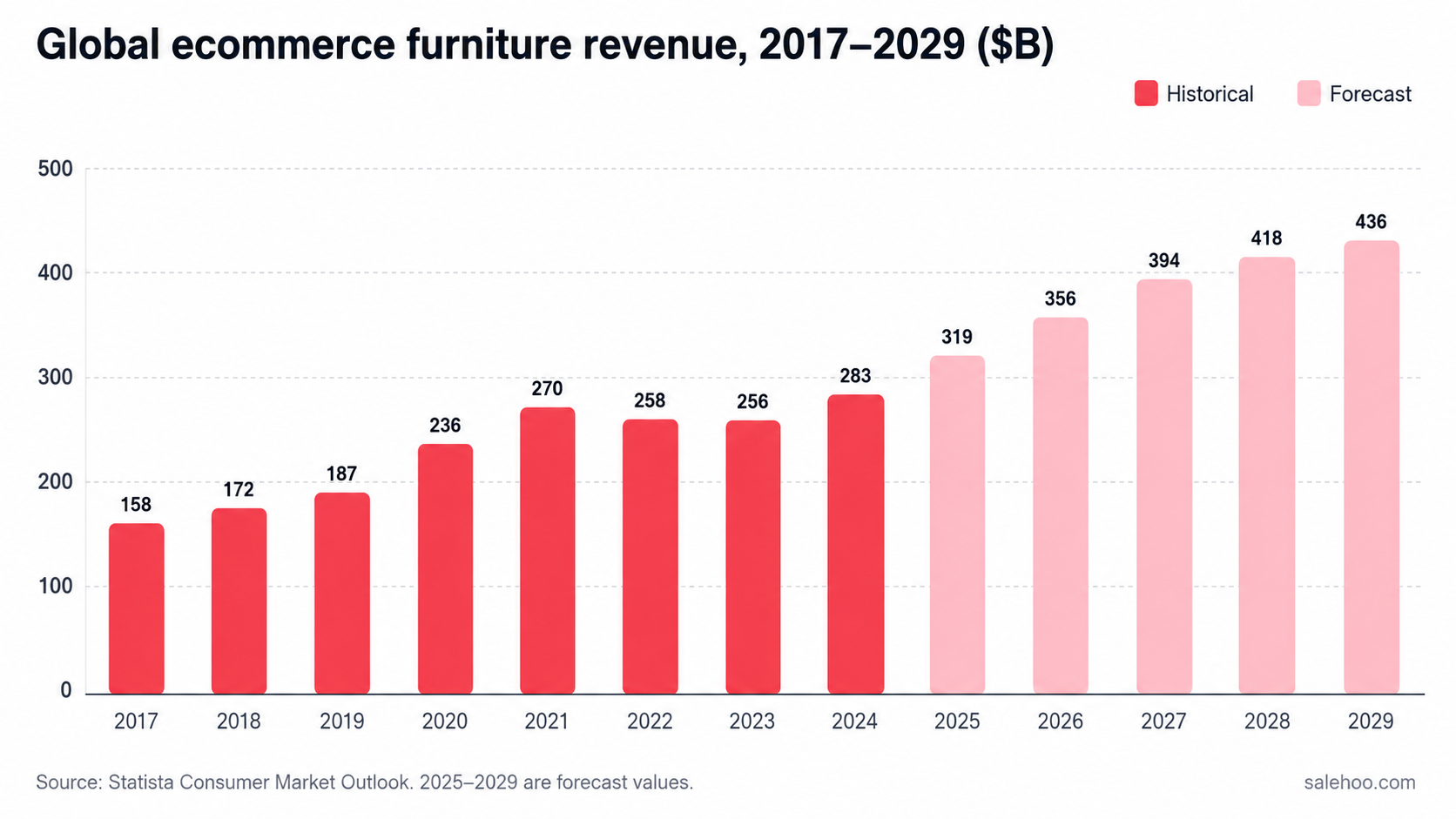

Global ecommerce furniture revenue hit $283.3B in 2024, is forecast to reach $318.5B in 2025, and is on track for $436.0B by 2029. That's average annual growth of around 8.2% from 2024 to 2029, slowing as the market matures toward the end of the decade.

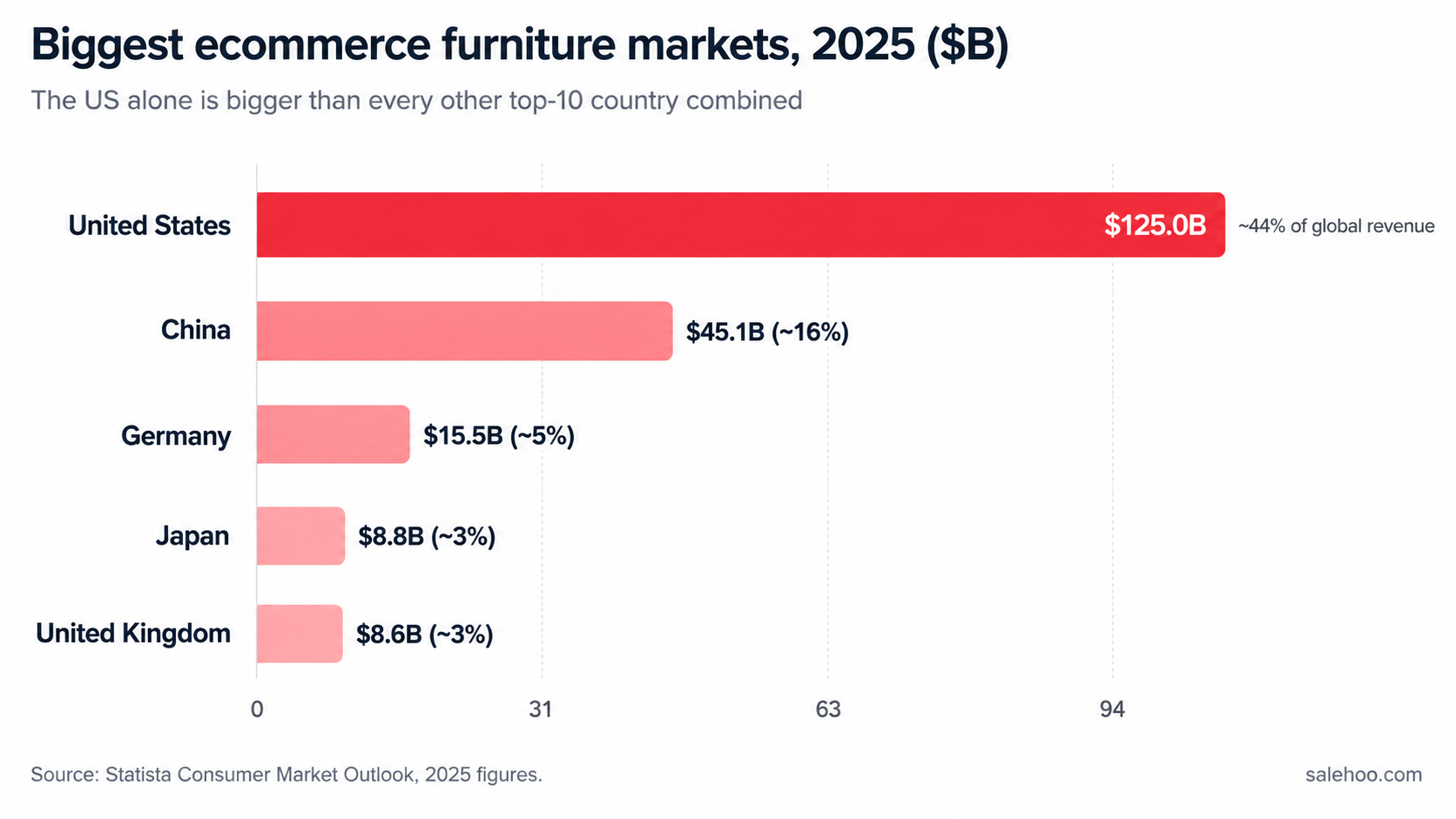

The United States is the largest single market by a wide margin at $125.0B in 2024, almost three times the size of China at $45.1B, the next biggest. Germany, Japan, and the UK round out the top five.

For sellers, the bigger story sits underneath the headline number. The pandemic-era buying spike is fully digested, growth is real but uneven, and the categories where independent sellers can actually compete are not the ones the press writes about. We'll get to all of that.

What this page covers (and why other sources say something different)

You'll find market-size estimates for ecommerce furniture that range from around $35B to $1.27T depending on the source. That gap isn't a typo, it's a definitional one. Before the numbers go anywhere useful, here's what this page is actually counting.

Scope of the $283.3B 2024 figure:

- Global retail ecommerce revenue from furniture (living room, bedroom, dining, office, outdoor)

- Includes mattresses and major upholstered goods

- Includes both marketplace-facilitated sales and direct retail ecommerce

- Excludes pure home decor accessories below the furniture line (rugs, lighting, wall art, soft furnishings) which are typically reported separately

- Excludes B2B/contract furniture sales channelled outside retail platforms

- Excludes secondhand and peer-to-peer sales

That's the same scope Statista uses in its Consumer Market Outlook, which is the underlying dataset most reputable estimates draw from.

Why other estimates differ:

| Source | What they measure | 2024 figure | 2029–2035 forecast |

|---|---|---|---|

| SaleHoo / Statista CMO scope | Global retail ecommerce furniture revenue | $283.3B | $436.0B by 2029 |

| Straits Research | Online furniture market, broader scope including some decor | $242.67B | ~$1.27T by 2033 |

| Business Research Company | Entire global furniture market (online + offline) | $750.6B | ~$791B in 2025, ~2–3% CAGR |

| Business Research Insights | Narrow "furniture ecommerce" report scope | ~$35B by 2026 | ~$51.6B by 2035 |

| CSIL Milano (World Furniture Outlook) | Real consumption growth across all channels | n/a (growth metric) | ~1.4% real growth 2025–2026 |

Global ecommerce furniture revenue, 2017–2029

The full decade-plus dataset.

| Year | Revenue ($B) | Annual change |

|---|---|---|

| 2017 | 158.4 | — |

| 2018 | 172.4 | +8.8% |

| 2019 | 186.8 | +8.4% |

| 2020 | 235.7 | +26.2% |

| 2021 | 269.7 | +14.4% |

| 2022 | 258.1 | −4.3% |

| 2023 | 256.4 | −0.7% |

| 2024 | 283.3 | +10.5% |

| 2025 | 318.5 | +12.4% |

| 2026 (forecast) | 356.3 | +11.9% |

| 2027 (forecast) | 393.9 | +10.6% |

| 2028 (forecast) | 418.0 | +6.1% |

| 2029 (forecast) | 436.0 | +4.3% |

Source: Statista Consumer Market Outlook, accessed June 2026. Historical years 2017–2024. Forecast years 2025–2029.

Compound annual growth (CAGR):

- 2017–2024 historical: ~8.7%

- 2024–2029 forecast: ~9.0%

That growth profile is unusual. Most categories that surged in 2020–2021 are still hangover-flat in 2024. Furniture corrected, then resumed an even faster pace than its pre-pandemic baseline.

From pandemic surge to recovery: what the timeline actually shows

The 2017–2029 trajectory has five distinct chapters, and each one tells you something different about the category.

2017–2019: steady-state ecommerce adoption. Annual growth between 8% and 9%. Furniture was a "future" category for online retail back then — the conventional view was that nobody would buy a couch they hadn't sat on. The numbers proved that wrong slowly.

2020–2021: the pull-forward. Sales jumped 26.2% in 2020 and another 14.4% in 2021. Lockdown spending plus the home-office build-out plus stimulus cheques compressed maybe five years of category adoption into 18 months.

2022–2023: correction. Revenue dipped slightly (−4.3% then −0.7%). That's not the category cooling. That's customers who'd already replaced everything not replacing it again.

2024: recovery. Up 10.5% to $283.3B. Slower than 2021's peak but well above the 2018–2019 baseline. The hangover is over.

2025–2029: re-acceleration, then maturation. Forecasts are double-digit through 2027 (peaking around +12% in 2025) and slow to single digits by 2028 and 2029 as the category approaches saturation in mature markets. Most of the late-decade growth will come from Asia Pacific and emerging markets, the US and Europe are already large enough that compounding gets harder.

A short editor's aside. In my experience watching SaleHoo's home and furniture supplier categories through this period, the 2022–2023 correction was actually a cleansing event. Suppliers who'd over-invested in pandemic-era SKUs got squeezed out. The ones still listed in our directory are the ones who survived the dip, which is part of why we think supplier vetting matters more in this category than almost any other. More on that later.

Biggest ecommerce furniture markets by country

Top five countries by online furniture revenue.

| Country | 2025 revenue ($B) | Share of global |

|---|---|---|

| United States | 125.0 | ~44% |

| China | 45.1 | ~16% |

| Germany | 15.5 | ~5% |

| Japan | 8.8 | ~3% |

| United Kingdom | 8.6 | ~3% |

Source: Statista Consumer Market Outlook, 2025 figures.

The US alone is bigger than every other top-10 country combined. That concentration matters when you're thinking about which market to target.

Regional outlook for sellers

North America is the deepest market by a wide margin, but also the most competitive and the most freight-sensitive. US sellers face elevated tariffs on furniture imports as of 2026, which has reshaped sourcing economics for anything coming from China. Near-shoring to Mexico and Vietnam has accelerated. Returns are expensive everywhere, but especially here because of average distances and dimensional weight pricing.

Asia Pacific is where the long-term growth is. China is the obvious heavyweight, but Indonesia, Vietnam, India, and the Philippines are growing faster than headline numbers suggest. The wrinkle for non-local sellers: cross-border ecommerce into Asia Pacific is regulatory-heavy, and category-specific rules (timber sourcing, flammability, labeling) trip up newcomers regularly.

Europe is split. Germany dominates and is mature. The UK is post-Brexit-tilted toward domestic sourcing for cost reasons. France and Italy have strong domestic furniture brands that crowd marketplaces. Eastern Europe is small but growing. EU regulations on chemical safety, FSC certification for timber, and end-of-life takeback are stricter than US equivalents. Plan compliance into the cost of goods.

Middle East and Africa is the fastest-growing region from a low base. UAE and Saudi Arabia in particular are seeing aggressive premium-segment growth driven by hospitality and new-build housing.

Latin America is mostly Brazil and Mexico. Both have meaningful ecommerce furniture demand but currency volatility and logistics infrastructure constrain margins for cross-border sellers.

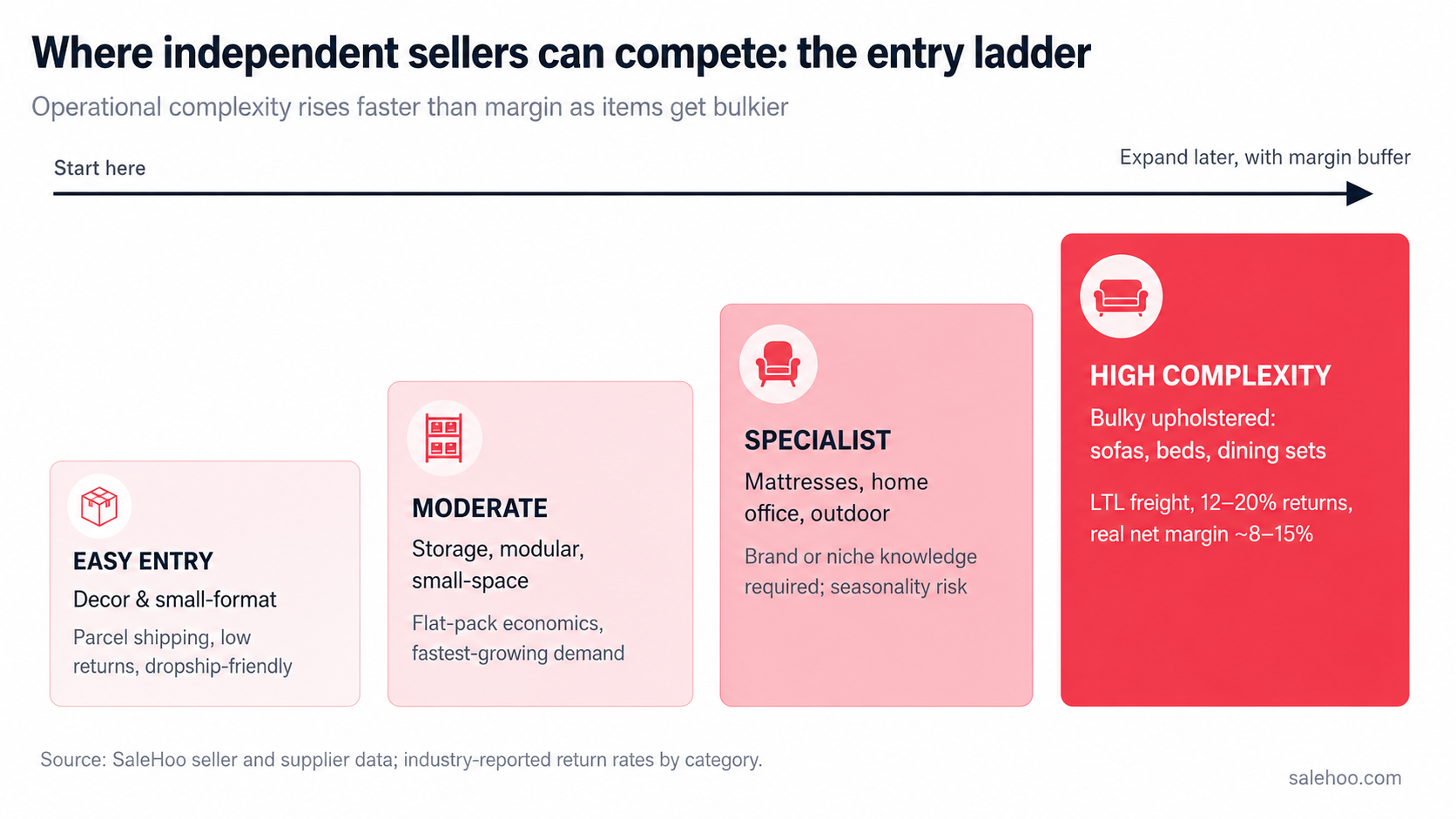

Where the seller opportunity actually is: by category

This is the part most market-size pages skip, and it's the part that actually decides whether selling furniture online is going to work for you.

Here's the honest seller triage, ordered from least painful to most.

Easy entry: decor-adjacent and small-format

Lamps, wall art, mirrors, throw pillows, decorative storage, small accent tables, plant stands, side tables. These ship in standard parcels, fit common dropshipping models, and forgive operational mistakes. Margins are tighter than bulky furniture per unit but the unit economics actually work because returns and damage rates are low. Most successful furniture-niche dropshippers we see start here. Browse home decor suppliers in the directory.

Moderate complexity: storage, organisation, modular

Storage units, modular shelving, small cabinets, foldable furniture, expandable dining tables. These are the categories Salsita's research flagged as growing fastest in 2026 — driven partly by the fact that the average US apartment has shrunk about 6% over the last decade per RentCafe, which permanently rewires what people are buying. Flat-pack shipping makes these economical to fulfill. Returns are higher than for decor but lower than for bulky upholstered goods.

Specialist category: mattresses

The bed-in-a-box model created a legitimate ecommerce mattress industry that wasn't there a decade ago. Margins on private-label mattresses are stronger than most furniture, customer acquisition is expensive, and the category is now crowded with well-funded DTC brands. If you can build a brand here you can do well. If you can't, the marketplace battle for generic mattresses is brutal. Browse mattress suppliers.

Specialist category: home office

The work-from-home build-out left a permanent uplift in home-office demand. Office chairs in particular kept growing through 2022–2023 when the rest of furniture corrected. Standing desks, ergonomic chairs, and small-footprint office furniture continue to perform. Browse office furniture suppliers.

Specialist category: outdoor and patio

Heavily seasonal. Heavily freight-sensitive (patio sets are bulky and damage-prone). Strong margins in the right SKUs but cashflow risk is real because of the seasonality. Browse outdoor furniture suppliers.

High complexity: living room and bedroom upholstered furniture

Sofas, sectionals, beds, dressers, dining sets. The headline category that newcomers assume is "ecommerce furniture." It's also the category where independent sellers struggle most. Reasons:

- Freight class is high. Shipping a sectional is genuinely expensive.

- Damage in transit is common and customer-paid resolution is rare.

- Return logistics are painful, you can't slap a return label on a 200-pound couch.

- The marketplace players (Wayfair, Amazon, Walmart, IKEA, JD.com) have crushing scale on these SKUs.

- Customer service load is heavy. Assembly questions, dimensional issues, delivery scheduling.

Browse sofa suppliers if you want a sense of what's available, but think hard about whether this is your first category.

Honest "approach with caution" notes

- Anything over 150 lbs that ships as one piece

- Anything with glass tops, mirrored surfaces, or fragile finishes

- Anything where assembly is non-trivial, the support cost compounds

- Custom upholstery without a tight supplier relationship, colour matches and timing slip constantly

The 2026 trends actually moving furniture inventory

Plenty of trend pieces this year. Most of them mash design aesthetics together with technology shifts and call it a list. Here's the version that matters if you're sourcing product.

1. AI search is reshaping discovery

Per Capgemini's consumer trends research, 58% of consumers now use generative AI tools instead of traditional search engines for product research. Furniture is one of the categories where this shift bites hardest because buyers ask "what's the best mid-century dining table under $800" exactly the way they'd ask a knowledgeable friend.

What it means for sellers: AI overviews and chat-based search are surfacing branded DTC players that have invested in structured product content. Marketplace listings with thin descriptions are getting cited less than they used to. Your product pages need clean specifications, clear materials, weight, dimensions, assembly time, and shipping detail, not just keyword-stuffed copy. The same content that converts on PDPs is the content AI engines quote.

2. Customisation is now the baseline expectation

In 2024, 45% of US kitchen renovation projects involved fully custom cabinets per Houzz. Not 5%. Forty-five percent. That expectation has bled into adjacent furniture categories. Buyers want to choose fabric, finish, configuration, dimensions.

What it means for sellers: pure dropship plays in furniture are getting harder unless the supplier supports basic configuration. Modular product lines beat fixed-SKU lines. If you're going wholesale, look for suppliers with at least colour and material options on the same base SKU.

3. Sustainability moved from claim to compliance

The eco-friendly furniture market is forecast to roughly double between 2024 and 2034, with surveys consistently showing around 68% of buyers willing to pay more for verifiably sustainable furniture.

What it means for sellers: vague "sustainable" claims now hurt you. Specific certifications (FSC for timber, OEKO-TEX for textiles, GREENGUARD for emissions) move conversion. Buyers cross-check on AI search.

4. Modular and small-space furniture is structural, not faddish

The apartment-shrinkage trend cited earlier isn't reversing. Urban housing in most developed markets keeps getting smaller, hybrid work keeps multi-purpose rooms relevant, and modular product lines let you sell to the largest addressable market with the smallest SKU count.

5. Comfort is now a measurable quality benchmark

Hybrid work permanently changed how people evaluate furniture. Buyers now treat ergonomics and long-session comfort as table-stakes for office chairs, sofas, beds, and accent seating. Generic "ergonomic" labels do nothing, measurable claims (cushion density, lumbar support depth, foam recovery rate) convert.

6. Social commerce is the second discovery channel

What it means for sellers: short-form video showing product in-room beats studio shots. 3D visualisation and AR try-on are increasingly expected on the PDP, not a bonus.

7. The aesthetic shift toward warmth and craft

Multiple designer surveys (1stDibs cited rattan and wicker at 27% mention rate for 2026) flagged the same set of design signals: warm dark woods (mahogany, walnut, cherry), cane and rattan, organic curves softening the 2024 oversized-sculptural look, decorative trim and edges, layered textiles. Less "Instagram showroom," more "lived-in and personal."

What it means for sourcing: if you've been building inventory around pale woods, smooth white finishes, and minimalist mid-century, the trend cycle has moved. The smart buy for 2026 isn't beige.

8. Tariffs and trade routes are reshaping supplier economics

This is the one most lists ignore. Higher US import tariffs on Chinese upholstered furniture have made near-shore production (Mexico, Vietnam, Indonesia) competitive on landed cost for the first time at scale. EU sellers face their own compliance lift around chemical safety regs.

What it means for sellers: if your sourcing strategy is "find the cheapest Chinese supplier," 2026 economics may surprise you. Diversified sourcing is no longer optional for US-facing sellers in furniture.

What it actually costs sellers: the risk side

Every other page on this SERP talks about growth. Almost none talk about why furniture chews up new ecommerce sellers. Here's the operator view.

Freight class and dimensional weight. Furniture ships LTL (less-than-truckload) once you cross certain size and weight thresholds, which moves you from parcel rates to freight rates overnight. A sectional that fits one calculation goes to a totally different one when the carrier reclasses it. Build a buffer of 15–25% over your initial shipping estimate.

Return rates and damage in transit. Industry-reported return rates on furniture sit roughly between 12% and 20% depending on category, well above ecommerce averages. Damage rates on bulky upholstered goods in transit are also higher than the category-blind statistics suggest. Refund-versus-replacement decisions on damaged $800 chairs eat margin fast.

Payment processor holds. PayPal and Stripe have a habit of holding funds on high-AOV new-seller accounts. I've seen a new SaleHoo member with a furniture store get their first $2,400 held for 21 days while PayPal "reviewed account activity." That's normal for the category. Plan working capital accordingly.

Supplier reliability and MOQ traps. Some furniture suppliers quote attractive unit pricing but require MOQs that lock up $5,000–$15,000 of cash on first order. Some advertise 7-day lead times that turn into 11 or 14 days once you place a real PO. Vetting is everything here. Our team has a process for vetting suppliers properly that we walk every directory listing through, and we get strict about it in furniture in particular.

Customer service load. Furniture customers ask more pre-sale questions and have more post-sale issues per order than almost any other category. Assembly help, missing hardware, colour-match disputes, delivery scheduling. Budget customer service capacity accordingly, or your reviews will sink the store. How to build ecommerce customer service that scales.

Margin compression on bulky goods. Headline category margins on big upholstered goods often look strong (30–40%). After freight, returns, damage, holds, and CS load, real net margins in the segment frequently land closer to 8–15% for independent sellers. The math is much friendlier at the decor and small-format end of the category.

Competitive landscape - who you're up against online

Knowing who else is selling the same product is half of category selection. The ecommerce furniture market has several distinct competitive tiers.

Mass-market marketplaces. Amazon, Wayfair, Walmart, Target Plus, JD.com, Coupang. Owns most of the bulky-furniture price-comparison search traffic. Independent sellers can win on these via private label or category specialisation, not by competing head-on on generic SKUs.

Big-box and warehouse retailers. IKEA, Home Depot, Lowe's, Costco. Tough to displace at the value end of the market. Their ecommerce arms are sophisticated and well-resourced.

DTC furniture brands. Article, Burrow, Castlery, Joybird, Floyd, Sundays, Maiden Home, and dozens more. Built on the bed-in-a-box and design-led playbook. Crowded, expensive to acquire customers, but profitable when the brand actually lands.

Specialist marketplaces. Chairish and 1stDibs for vintage and mid-to-high-end. Etsy for handmade and small-batch. AptDeco and Kaiyo for resale. Different competitive dynamics, different acceptance criteria.

Independent ecommerce stores and Shopify-native brands. Where SaleHoo members usually compete. The winners pick a defensible niche; a category, an aesthetic, a regional focus, a customer profile and build around it instead of trying to be all things to all buyers.

Where independents actually win: specialisation (one room, one style, one customer), premium product photography, fast and accurate customer support, and being good at the small unit economics most marketplaces ignore. Going head-to-head with Wayfair on price is not a strategy. Owning "the best place online to buy small-space dining sets for studio apartments" is.

Should you sell furniture online in 2026?

Honest answer: yes if you fit one of these profiles, probably not if you don't.

Good fit:

- You can start with home decor, small-format, or modular and let the bulk-furniture decision come later

- You're willing to do supplier vetting properly and not chase headline-low unit prices

- You can budget for higher returns and freight than typical ecommerce

- You have working capital tolerance for occasional processor holds

- You want a category with high AOV, strong demand, and broad demographic reach

- You're prepared to specialise rather than compete on breadth

Probably not the right fit:

- You want to start with sectionals because the AOV is attractive

- You're cashflow-tight and can't absorb a $1,500 freight-damage write-off in month one

- You're operating thin-margin marketplace listings with no brand layer

- You don't have the customer-service bandwidth for high-touch product

The path that works for most SaleHoo members: start with decor or small-format, build supplier relationships and operational rhythm, then expand into bulkier categories with margin to absorb the freight and returns reality. We've walked through this trajectory with thousands of members. The pattern is consistent.

If furniture isn't the right starting point, there are better categories to begin with. Our piece on underrated niches covers some of them.

How SaleHoo members source furniture and home decor

This is the section where I should tell you what we actually do, since the rest of the page has been pretty hard on the category.

SaleHoo's directory includes hundreds of pre-vetted suppliers across the furniture and home decor categories. Several supplier types matter for furniture specifically:

- General home decor and furniture suppliers for sellers building broad ranges (look at home decor and the broader home category)

- Mattress and bedding specialists (mattresses, bedding)

- Office furniture specialists for the post-hybrid demand (office furniture, office chairs)

- Outdoor and patio (outdoor furniture, patio furniture)

What our vetting catches in furniture specifically — and why this matters more here than in most categories:

- Quoted lead times versus actual lead times. Furniture suppliers are especially prone to optimistic lead-time quotes that slip in production.

- MOQs that aren't disclosed until quote stage

- Freight classification accuracy

- Returns and damage policy clarity

- Whether the supplier is the actual manufacturer or a reseller in front of one

Our broader guide to choosing suppliers walks through this in more detail, and the dropshipping versus wholesale comparison helps you decide which sourcing model fits the category you're chasing.

If you want to start sourcing now, browse the supplier directory.

FAQs

About $318.5B in forecast 2025 revenue, up 12.4% from $283.3B in 2024, per the Statista Consumer Market Outlook dataset.

$436.0B by 2029. Average annual growth of around 9% from 2024–2029, slowing in the last two years as mature markets approach saturation.

The United States, at $125.0B in 2024 — roughly 44% of the global total. China is second at $45.1B.

Different sources measure different things. Some count only retail ecommerce; some include the entire furniture market (online and offline); some include home decor in the scope; some don't. The figures cited on this page use the Statista CMO scope: global retail ecommerce furniture revenue.

It can be, but margin is category-dependent. Decor and small-format goods deliver more realistic net margins for independent sellers than bulky upholstered furniture, where freight and returns compress margins faster than headline numbers suggest. Picking the right entry category matters more than picking the "right" trend.

Freight class re-classifications, return and damage rates above ecommerce averages, payment processor holds on high-AOV new-seller accounts, supplier MOQ traps, and customer-service load on assembled goods.

Home office, modular and small-space furniture, sustainable and certified-material furniture, and decor-adjacent categories. Mattresses continue to grow but the segment is crowded with well-funded DTC brands.

In practice the terms get used interchangeably, but research firms sometimes draw a distinction. The first usually refers to all furniture sold via online retail channels. The second sometimes refers to a narrower segment of furniture-specific ecommerce platforms or pure-play online retailers. Always check the source's scope definition before comparing numbers across reports.

Mass marketplaces (Amazon, Wayfair, JD.com, Walmart), big-box retailers (IKEA, Home Depot, Costco), specialist marketplaces (Chairish, 1stDibs), and a fast-growing DTC tier (Article, Burrow, Castlery, Joybird, and dozens of category-specific brands).

About 58% of consumers now use generative AI tools for product research per Capgemini. AI overviews prefer cleanly structured product content with explicit specifications. Sellers with thin marketplace descriptions get cited less than they used to. Detailed PDPs are now an AI-search signal as much as a conversion lever.

About this article

About the author

)