Quick answer.

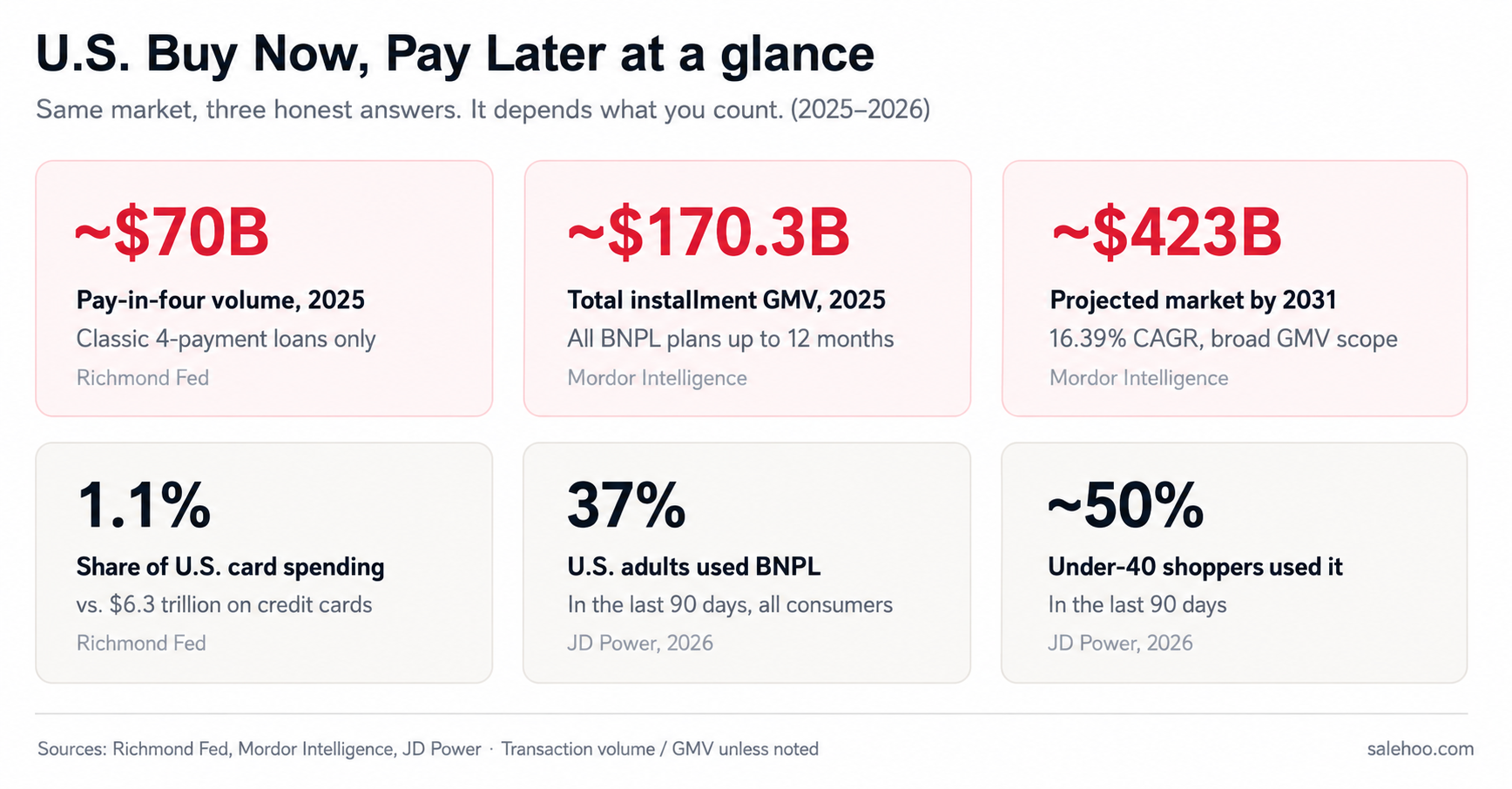

There's no single "U.S. BNPL market size," and that's the first thing nobody tells you. It depends on what you count. The narrow, strictest measure (classic pay-in-four loans) sat around $70 billion in transaction volume in 2025, per the Federal Reserve Bank of Richmond. Broader measures that fold in every installment plan up to 12 months put the market closer to $170 billion in 2025, heading toward $423 billion by 2031 (Mordor Intelligence). And if you only count what providers earn in fees, the number drops to a couple billion. Same market. Three honest answers. Below, we untangle which one you actually want, and what it means if you're deciding whether to add BNPL to your own store.

Buy Now, Pay Later went mainstream while a lot of store owners weren't looking. About half of Americans have now used it for online purchases, and among shoppers under 40, half used it in just the last three months. So the real question for a seller isn't "is BNPL big." It's big. The question is which number to trust, and whether it's worth turning on at your checkout.

Let's do both.

How big is the U.S. BNPL market?

Pick your definition first, then the number follows.

If you mean the classic pay-in-four product (four interest-free payments, no hard credit check), the Federal Reserve Bank of Richmond estimated roughly $70 billion in U.S. transaction volume for 2025. To put that in scale, the Fed notes that's only about 1.1% of total U.S. credit card spending, which topped $6.3 trillion. BNPL feels everywhere. It's still a sliver of how Americans actually pay.

If you mean the whole installment market, including longer plans and bank-issued versions, the figure is much larger. Mordor Intelligence values the U.S. BNPL services market at about $170.32 billion in 2025, growing to $198.21 billion in 2026 and a projected $423.08 billion by 2031 (a 16.39% CAGR). That's gross merchandise value, the total worth of goods bought through these plans, not provider revenue.

And if you mean what BNPL companies earn, Grand View Research pegged provider revenue at $1.64 billion in 2022, forecasting $9.20 billion by 2030.

None of these is wrong. They're measuring different things. Most articles just grab one and call it "market size," which is exactly how readers end up confused. Here's the part most people miss: the gap between $70B and $170B isn't a mistake, it's a definition.

U.S. BNPL at a glance (2025–2026)

| Metric | Figure | What it measures | Source |

|---|---|---|---|

| Pay-in-four transaction volume (2025) | ~$70 billion | Classic 4-payment loans only | Richmond Fed |

| Total installment market (2025) | ~$170.3 billion | All BNPL/installment GMV ≤12 mo. | Mordor Intelligence |

| Projected market by 2031 | ~$423 billion | Broad GMV scope | Mordor Intelligence |

| Share of total credit card spending | ~1.1% | Pay-in-four vs. card volume | Richmond Fed |

| U.S. adults who used BNPL in last 90 days | 37% | All consumers | JD Power, 2026 |

| Under-40 shoppers who used it in 90 days | ~50% | Consumers under 40 | JD Power, 2026 |

| Fastest-growing category | Healthcare (~19.9% CAGR) | By end-use | Mordor Intelligence |

| Most-used provider | PayPal (56% of BNPL users) | By usage | LendingTree, via Richmond Fed |

Why every source gives a different BNPL number

This is the section that should make you trust the rest of the page. Four different ways to measure the same market, and each produces a wildly different headline.

1. Pay-in-four loans only. The strict definition. A short-term, no-interest loan split into four payments over six weeks, first payment at checkout. No hard credit pull, and providers usually don't report it to credit bureaus. The Richmond Fed sizes this at about $70 billion for 2025. It's the cleanest "BNPL" number because it excludes longer, interest-bearing financing that behaves more like a regular loan.

2. Total installment GMV. The broad definition. This counts the full value of everything bought through any short-term installment plan, including bank programs like Mastercard Installments and longer plans up to 12 months. That's how Mordor reaches $170 billion. Bigger scope, bigger number.

3. Provider revenue. What Klarna, Affirm, and the rest actually book in fees and interest. A fraction of the money flowing through, so you get small figures like Grand View's $1.64 billion.

4. Payment volume / forecast models. Various analysts model future "payment volume" off adoption curves, which is where you see year-by-year projections that climb into the $100B+ range.

Mordor put it plainly in its own methodology: published estimates diverge because some firms count provider fee revenue, others count GMV, and they refresh their data on different schedules. So when you see "$2 billion" on one site and "$170 billion" on another, neither is lying. They're answering different questions. The trick is knowing which question you're asking.

For a shopper or a seller, the number that usually matters is transaction volume (how much is being spent this way), which is why we lead with the Fed's pay-in-four figure and the broader GMV figure side by side, instead of pretending there's one true answer.

Estimates by source, side by side

| Source | What it measures | Base figure | Forecast |

|---|---|---|---|

| Richmond Fed (2026) | Pay-in-four transaction volume | ~$70B (2025) | ~20%/yr growth trend |

| Mordor Intelligence (2026) | Total installment GMV | $170.32B (2025) | $423.08B by 2031 |

| Grand View Research | Provider revenue | $1.64B (2022) | $9.20B by 2030 |

| Payment-volume model | Forecast payment volume | ~$97.3B (2025) | ~$124.8B (2027) |

U.S. BNPL by the numbers

The clearest hard data we have comes from the Consumer Financial Protection Bureau, which pulled actual loan files from the six biggest providers (Affirm, Afterpay, Klarna, PayPal, Sezzle, and Zip). The Richmond Fed summarized it like this.

| Year | Loans originated (millions) | Dollar volume (billions) | Average loan size |

|---|---|---|---|

| 2019 | 19.8 | $2.2 | $111 |

| 2020 | 77.9 | $8.9 | $114 |

| 2021 | 196.6 | $25.5 | $129 |

| 2022 | 273.8 | $33.4 | $122 |

| 2023 | 335.8 | $43.9 | $131 |

Two things jump out. First, the explosive pandemic-era growth has cooled into a steadier pace, roughly 31% a year between 2021 and 2023, then around 20% a year in real terms since. Still fast. Just not the rocket it was in 2020. Second, look at that average loan size: about $131. BNPL isn't financing yachts. It's splitting up a $130 order. That detail matters a lot when we get to whether it fits your store.

For the broader payment-volume view that many ecommerce reports cite, U.S. BNPL payment volume is often modeled in the range of $97 billion for 2025 rising toward $125 billion by 2027. We flag it as a forecast model, not gospel, precisely because of the definition problem above.

Who's actually using BNPL?

Adoption is the part that's hard to argue with, because multiple independent surveys land in the same place.

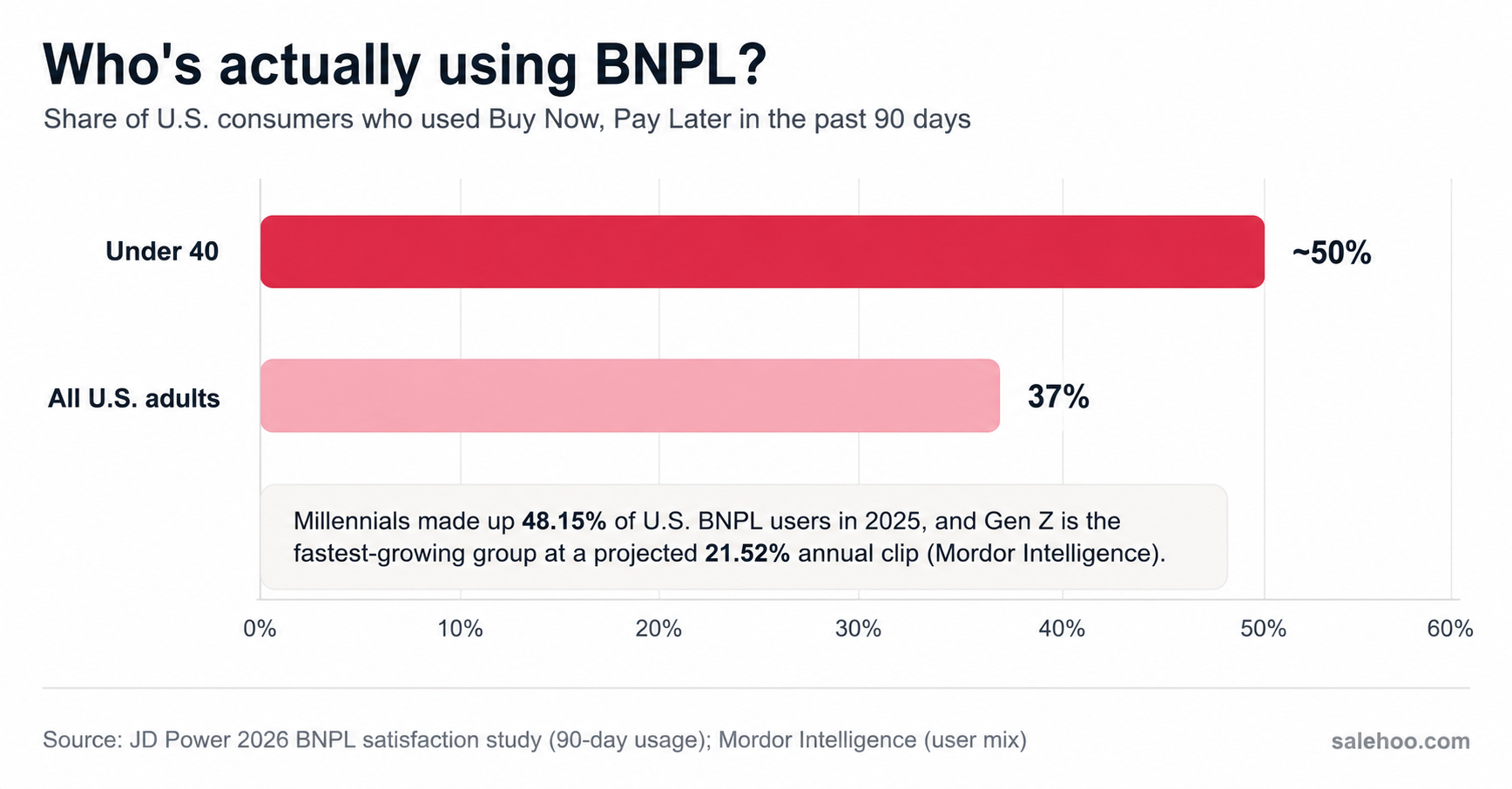

JD Power's 2026 study found 37% of U.S. consumers used BNPL in the past 90 days, up five points in a single year. Among under-40 shoppers, that figure was about 50%. A Gallup survey reported roughly half of all Americans have used it for online purchases at some point, with 10% using it frequently.

It skews young, and it skews toward people feeling cash-flow pressure. Mordor found millennials made up 48.15% of U.S. BNPL users in 2025, with Gen Z the fastest-growing group at a 21.52% projected annual clip. The ABC/Gallup reporting added a sharper note: Americans who said they don't have enough money to live comfortably were nearly three times as likely to use installment plans online. That's not a knock on BNPL. It's a clue about who clicks it, and it should shape how you'd present it in your own store.

If your customers are Gen Z and millennial, BNPL isn't a nice-to-have to them. It's an expectation at checkout.

Top U.S. BNPL providers (and which ones fit a small store)

The big dedicated names are Affirm, Afterpay (Block), Klarna, PayPal, Sezzle, and Zip. The newer story is that banks and card networks muscled in. Chase, American Express (Plan It), and Citi (Flex Pay) all run installment features now, and JD Power found bank-brand satisfaction (704 on a 1,000-point scale) has pulled ahead of fintech BNPL brands (603).

Here's the merchant-eye view, not the investor view.

| Provider | Type | Typical fit for sellers | Worth knowing |

|---|---|---|---|

| PayPal Pay in 4 | Fintech / wallet | Easiest add if you already use PayPal | Most-used BNPL provider; low friction for existing PayPal merchants |

| Afterpay | Fintech | Strong with fashion, beauty, younger shoppers | Pay-in-four focus; deep Shopify integration |

| Klarna | Fintech | Broad retail; big marketing reach | Offers pay-in-four and longer financing; large shopper base |

| Affirm | Fintech | Higher-ticket items, electronics, furniture | Began reporting loans to credit bureaus in 2025; longer terms can carry interest |

| Sezzle | Fintech | Smaller merchants, budget-conscious buyers | Optional credit-bureau reporting |

| Zip (Quadpay) | Fintech | Flexible across categories | App-based, works across many retailers |

| Chase / Amex / Citi plans | Bank | Customer-side, not merchant integration | Highest satisfaction scores; mostly post-purchase plans on existing cards |

A real consideration most "best BNPL" lists skip: a chunk of installment activity now happens after purchase, on a credit card the shopper already has. JD Power found 52% of card fixed-payment-plan decisions happen after the purchase, reviewing the bill, versus 48% at checkout. Translation for you: even if you never add a BNPL button, some of your customers are already splitting up their payment on the back end. Adding it at checkout mostly affects conversion, not whether BNPL "happens."

What's driving the growth

A few forces, briefly, because you came here for numbers, not a thesis.

Younger shoppers prefer interest-free installments to revolving credit card balances. Mordor found close to 46% of Gen Z used a BNPL option in 2025. Merchants like the conversion math (more on that below). Embedded checkout integrations made it one-tap easy. And card networks plus banks bolted installment features onto cards millions of people already carry, which widened the on-ramp overnight. BNPL also spread beyond retail: healthcare is the fastest-growing vertical, and travel saw a 289% jump in BNPL booking volume in 2024, with installment users spending about 70% more per trip.

That last stat is the seller's hook, so let's hold it for the section that actually matters to you.

The honest part: risks, defaults, and regulation

A page that only cheerleads BNPL isn't worth your time. Here's the balanced read.

On the system level, BNPL looks healthier than the headlines suggest. The Richmond Fed found the charge-off rate on BNPL loans was 1.83% in 2023, lower than the 4.19% on credit cards in late 2023. Total BNPL debt outstanding at any given moment is around $3.02 billion, against $1.23 trillion in credit card debt, roughly 400 times smaller. Even deep-subprime borrowers, who made up a large share of originations, still repaid their loans about 96% of the time. So the "BNPL is a debt bomb" framing isn't well supported by the data, at least not yet.

On the consumer level, though, the cracks are real. LendingTree's 2025 survey found 41% of BNPL users made at least one late payment in the past year, up from 34%. A Bankrate survey found nearly half of users ran into problems like overspending, missed payments, or regret. Bankrate's Ted Rossman frames it well: used right, BNPL is a cash-flow tool; used wrong, it's an easy way into more debt than you meant to take on. His rule of thumb is that it works for occasional necessary big-ticket buys, not for routine spending on gas, groceries, or food delivery. Worth noting too: the longer, interest-bearing BNPL plans can carry rates comparable to credit cards, so the "interest-free" reputation only applies to the classic pay-in-four version.

Regulation is the wildcard. The CFPB moved in 2024 to treat certain BNPL loans like credit cards, then signaled in 2025 it wouldn't prioritize enforcement while it reviews the rule. States like New York and California are weighing their own disclosure rules. And the credit-reporting question is live: Affirm began reporting BNPL loans to the credit bureaus in 2025, while Klarna and Afterpay have been cautious about it. None of this is settled, which is why we date-stamp it: this reflects the picture as of early 2026.

What BNPL growth means for your store

This is the part the market-research firms can't write for you, because they're selling reports, not running stores. So let's get practical.

Should you offer BNPL at checkout?

The case for is mostly about conversion and order size. Mordor reports that retailers enabling installments see conversion lifts of 20-30% and average-order-value gains of 30-50%. Those are big numbers, and they're the reason BNPL spread so fast. When a $180 jacket reads as "4 payments of $45," more carts make it to checkout, and some shoppers trade up.

But, and this is the part the conversion stats hide, BNPL costs you. The merchant fee on a BNPL transaction typically runs higher than a standard card processing fee, often in the 3-6% range depending on provider and volume. If your margins are thin, that fee can eat the upside fast.

When BNPL is probably worth it

- You sell higher-consideration items: that $130 average loan size tells you BNPL shines on orders north of, say, $75-$100, not on a $12 phone case.

- Your buyers are young: Gen Z and millennial-heavy stores see the biggest checkout effect.

- You're in a category where it's normalized: fashion, beauty, electronics, home and furniture, fitness equipment. Fashion and apparel alone were 27.85% of the U.S. BNPL market in 2025.

- Your margin can absorb the fee and still come out ahead on the conversion lift.

When it's probably not worth it

- Low average order value. Splitting a $20 order into four payments adds fee cost and friction for almost no conversion gain.

- Thin margins. If you're running 10-15% net, a 5% BNPL fee is a serious bite. Run the math before you switch it on.

- High return-rate categories. BNPL plus easy returns can mean refunds, partial-payment reversals, and reconciliation headaches. More on that in a second.

A 60-second provider checklist

Before you flip it on, get answers to these:

- What's the all-in merchant fee, including any fixed per-transaction charge?

- How fast do you get paid, and do you get the full amount upfront or as the customer pays?

- Who eats the risk if the customer defaults? (With most pay-in-four providers, it's them, not you, which is the point.)

- How do returns and partial refunds work against the installment schedule?

- Does it integrate cleanly with your platform, or is it a clunky bolt-on? (If you're on Shopify, check the native options first.)

The smartest way to find out is to turn it on for one category or one 30-day window, watch your AOV, conversion, and net margin, then decide. Don't roll it across the whole store on faith.

If you're still sorting out your checkout stack, our guide to payment gateways for dropshipping and PayPal alternatives covers the options. And if the real lever for you is selling higher-margin, higher-AOV products where BNPL actually pays off, that starts with finding the right products and reliable suppliers.

Frequently asked questions

It depends what you count. Classic pay-in-four volume was about $70 billion in 2025 (Richmond Fed), the broader installment market about $170 billion and climbing toward roughly $200 billion in 2026 (Mordor Intelligence). Provider revenue is far smaller, in the low billions.

Because sources measure different things. Some count only pay-in-four loans, some count all installment GMV up to 12 months, and some count what providers earn in fees. Refresh schedules differ too. Same market, different definitions.

Both exist, which is the confusion. Most "market size" figures you'll see are transaction or payment volume (GMV). Provider-revenue figures are much smaller and measure company income, not consumer spending.

Roughly half have used it for online purchases (Gallup). JD Power found 37% used it in the last 90 days, and about 50% of under-40 shoppers did.

Affirm, Afterpay, Klarna, PayPal, Sezzle, and Zip lead the dedicated space, with PayPal the most widely used. Banks and card networks (Chase, Amex, Citi) have added their own installment plans.

Fashion and apparel (the largest single category), electronics, home and furniture, beauty, plus fast-growing healthcare and travel. Higher-ticket, higher-consideration purchases see the biggest effect.

If your average order is above ~$75-$100, your buyers skew young, and your margin can absorb the merchant fee, it's usually worth testing. For low-AOV or thin-margin stores, it often isn't. Test one category for 30 days before committing.

Merchant fees that can erode thin margins, return-and-refund reconciliation against installment schedules, and the chance that easy financing nudges buyers who later regret the purchase, which can feed returns.

This article is general information for online sellers, not financial or legal advice. Run your own numbers, and check current provider terms before adding BNPL to your store.

About this article

About the author